August 3, 2025

Swiss Watch Brand Rankings: 2015–2024 Performance

Over the past decade, the Swiss watch industry has undergone significant shifts, some expected and others surprising. Using insights from Morgan Stanley and LuxeConsult, this post examines which brands have gained ground, which have remained dominant, and how evolving consumer preferences are transforming the market.

Over the past decade, the Swiss watch industry has undergone significant shifts, some expected and others surprising. Using insights from Morgan Stanley and LuxeConsult, this post examines which brands have gained ground, which have remained dominant, and how evolving consumer preferences are transforming the market.

Who Ranks the Watch Industry and How?

Every year, Morgan Stanley and LuxeConsult collaborate to publish the most referenced report on Swiss watch brand performance. Their rankings are based on a combination of export data from the Federation of the Swiss Watch Industry (FH), estimates from group disclosures (such as Swatch Group or Richemont), and insights from retail channels. Although not officially audited, the data provides a clear view of unit volumes, revenue (CHF), and market share (both in value and prestige).

These reports provide a rare glimpse into an otherwise private and closely guarded industry.

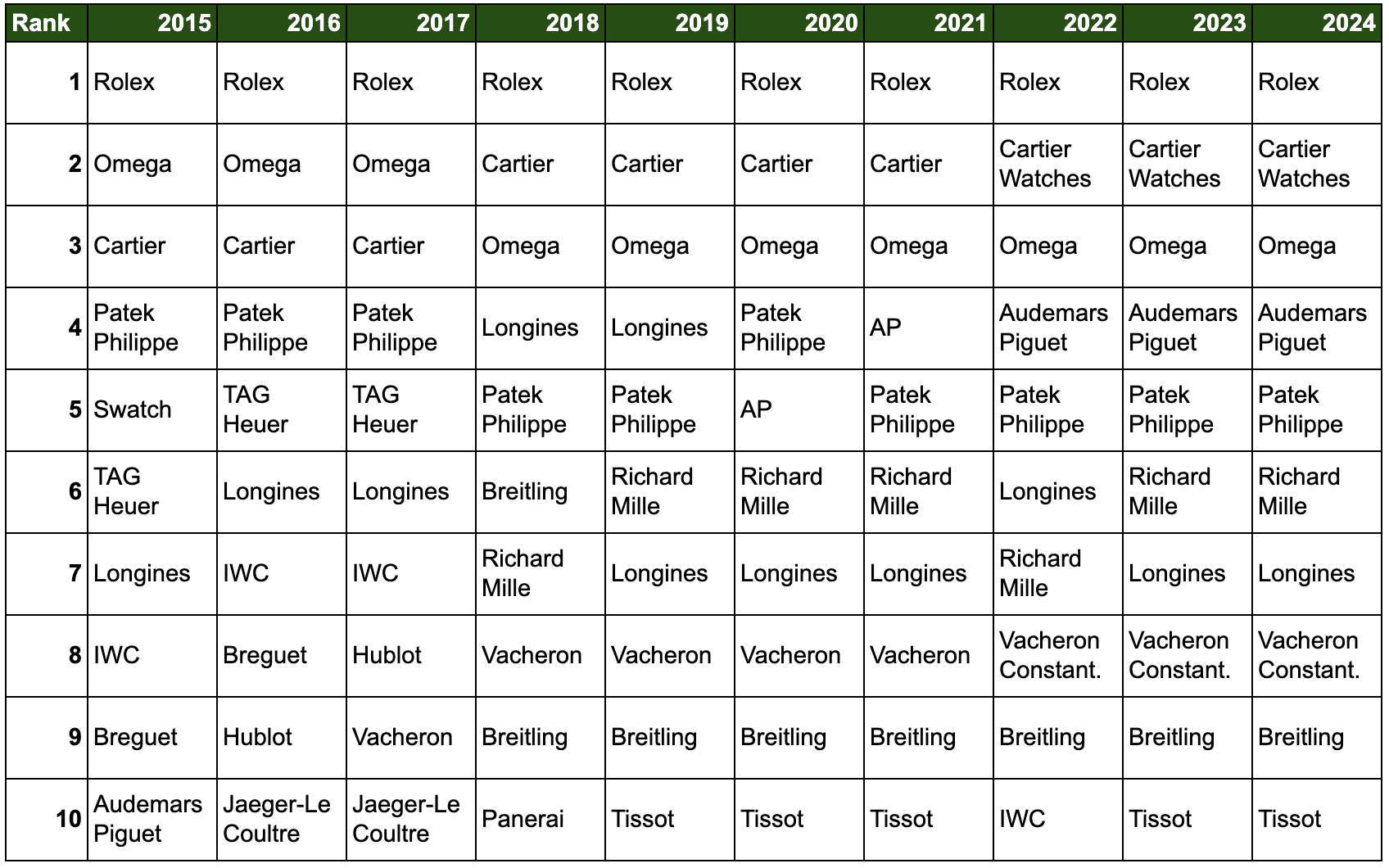

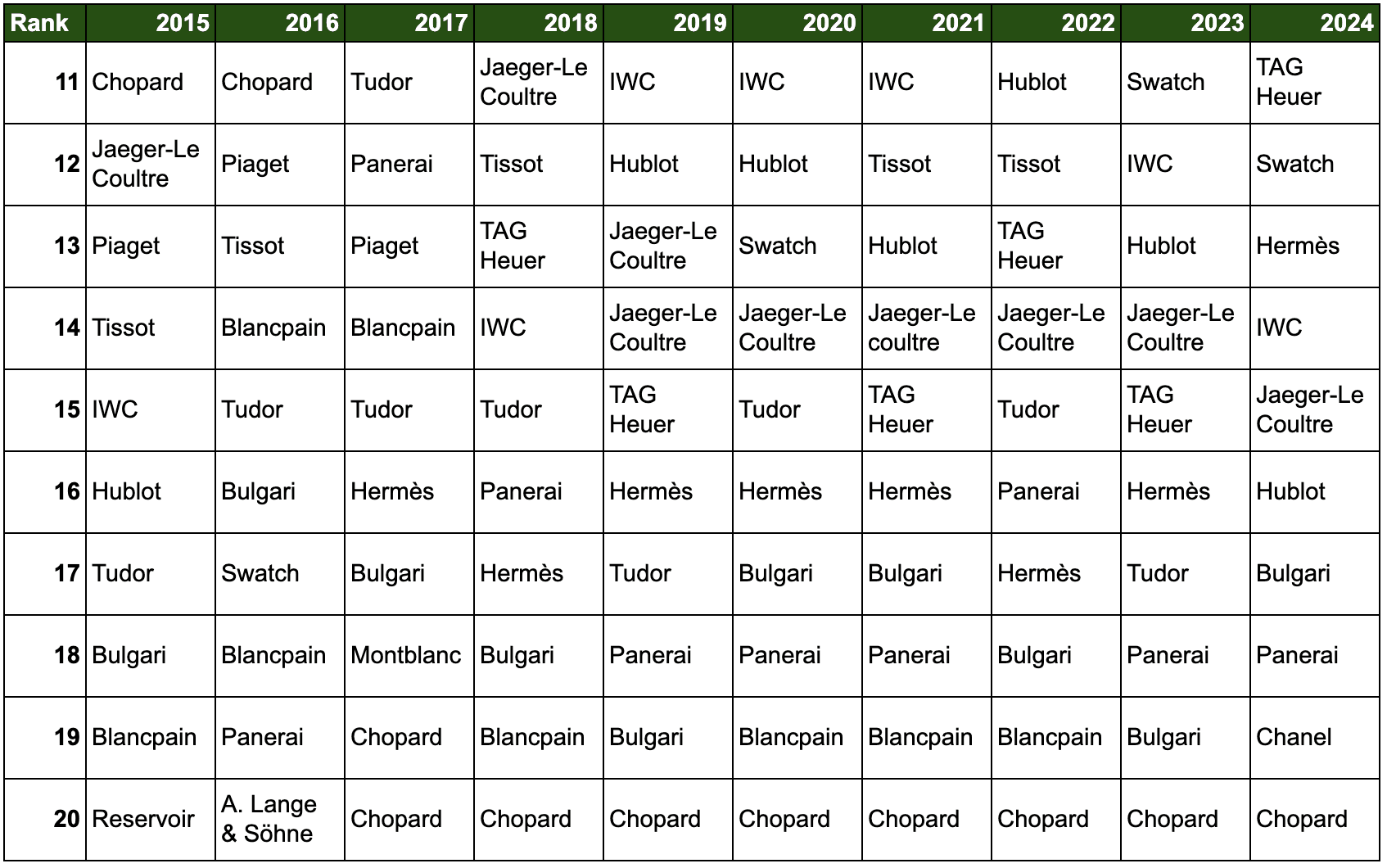

Below you can find the Top 20 Swiss Watch Brands by Sales Rank (2015–2024)

The Big Four: Who Dominates the Top?

Across the decade, four brands steadily held the high ground:

- Rolex

- Patek Philippe

- Audemars Piguet

- Richard Mille

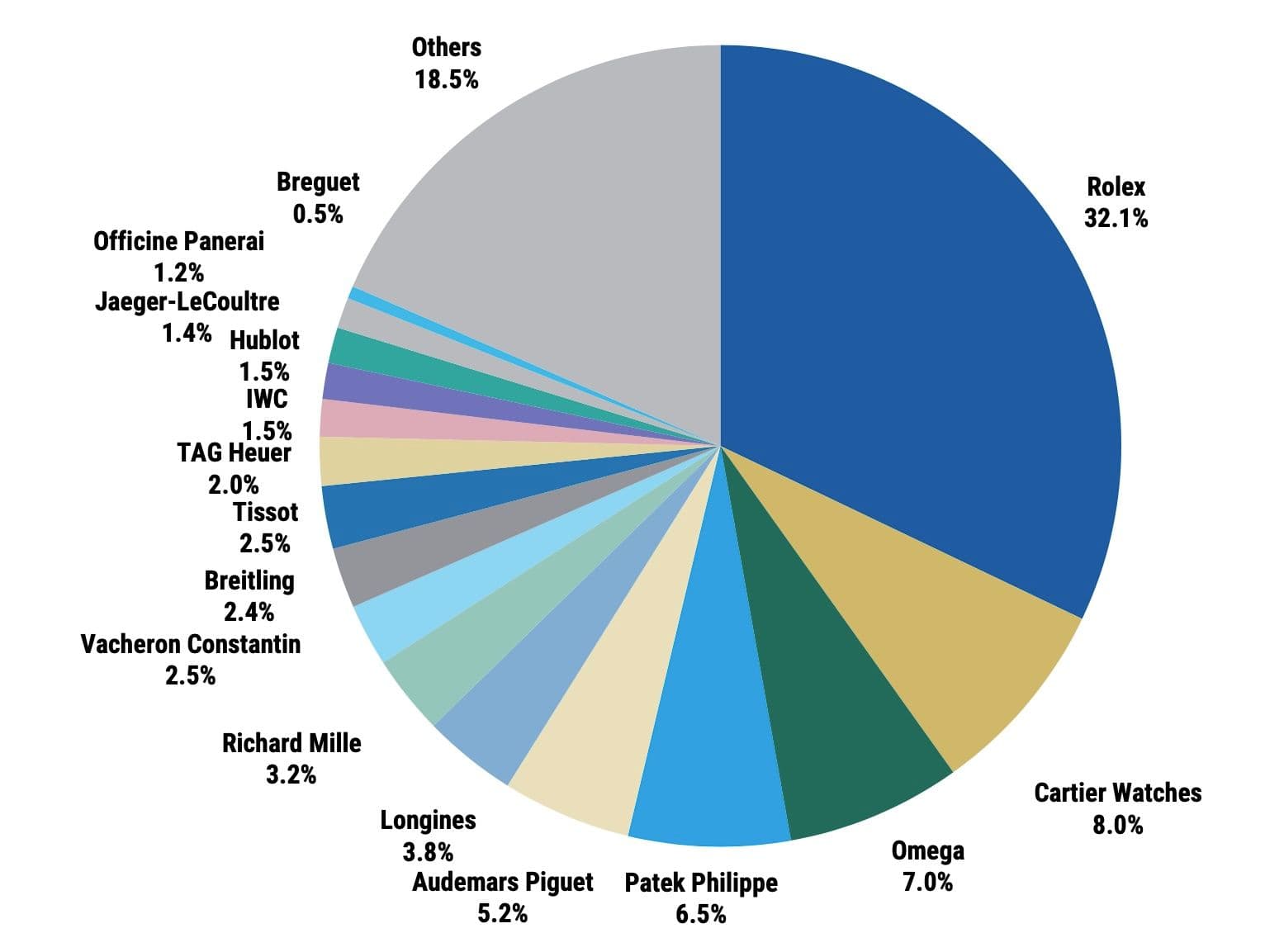

By 2024, these four brands, collectively called “The Big Four,” held nearly 50% of the market share by value despite low production volumes. Notably, none of them are part of major watch groups, which sets them apart from other top 20 players.

Each brand has a distinct strategy. Rolex stands out through vertical integration and scarcity tactics, while Patek Philippe is renowned for its ultra-high horology. Audemars Piguet emphasizes its Royal Oak line and direct sales model, whereas Richard Mille is recognized for its exclusivity and technological innovation.

Volume Workhorses and the Squeezed Middle

Brands like Tissot, Longines, and TAG Heuer have long dominated the Swiss watch industry in terms of production volume, each regularly shipping over one million watches annually. They are the essential workhorses of the export economy, supporting extensive global distribution and broad accessibility.

While Tissot and Longines lead in shipment numbers, they lag behind in revenue rankings. Conversely, Patek Philippe and Audemars Piguet, producing fewer than 110,000 units combined annually, consistently rank among the top five brands by revenue.

In the changing world of luxury watchmaking, the role of workhorses has become more uncertain. Today, they find themselves in what many call the squeezed middle: too premium to win on price, too mainstream to command exclusivity.

Despite their size and heritage, they face increasing pressure from both smartwatches (which dominate the lower end) and microbrands and independents, who excel in storytelling, scarcity, and direct-to-consumer appeal.

However, while independent brands lead the value rankings, conglomerates like Swatch Group and Richemont still support volume, with mixed results in shifting their portfolios toward the high-end.

Evolving Players: From Midfield to Luxury Podium

While the top positions stayed steady, several brands quickly climbed the rankings.

- Hermès: Rising from outside the top 20 to top 13 by 2024, driven by its H08 and focus on in-house mechanical credibility.

- Tudor: Rolex’s sister brand rode the Black Bay wave but experienced volatility in recent years.

- Swatch: The 2022 launch of the MoonSwatch brought the brand back into relevance and retail visibility.

These movements underscore how a single product launch can dramatically alter brand perception, even in a heritage-driven industry. It’s exciting to see how a single release can make such a significant impact.

Resilience and Realignment: Where Swiss Watchmaking Stands Today

The COVID-19 pandemic sent shockwaves through the Swiss watch industry. In 2020 alone, exports dropped by over 30% in unit terms, marking the sharpest decline in decades. Brands that depended on travel retail, mid-tier volume, or physical boutiques faced immediate pressure. Production slowed, distribution fractured, and demand became more polarized.

But out of disruption came a shift in perception. Consumers began prioritizing value retention, brand integrity, and craftsmanship over sheer accessibility. This accelerated the rise of what many now call the “value champions”, brands like Rolex, Patek Philippe, and Audemars Piguet that combine scarcity with long-term desirability.

Today, the Swiss industry operates in two distinct lanes:

- On one end, volume brands focus on reach and affordability.

- On the other hand, low-volume luxury makers dominate attention, resale value, and prestige.

As we look ahead, this two-speed model is likely to intensify. The middle ground is thinning, and brands must now choose: scale or scarcity, broad appeal or elevated position. The industry has proven its resilience, but the rules have changed.

From Rolex’s untouched reign to the surprise re-entry of Swatch, the last decade has been anything but static. The industry’s heartbeat now depends on scarcity, storytelling, and strategic drops, not just traditional prestige.

If you want to understand where watches are going, don’t just follow the money. Follow the momentum. The next decade will belong to those who master scarcity, innovation, and emotional relevance.

References:

Share this piece

Send it to another watch nerd.

Keep reading

Related articles

June 12, 2026

Makina's Cassiel II Shows a Brutalist Chronograph Can Feel Deliberate Instead of Costume-Like

June 12, 2026

Longines' Master Collection Finally Feels Like a Complete Dress-Watch Platform Instead of a Single Safe Compromise

June 11, 2026

Blancpain's New Fifty Fathoms Tech Makes a Specialist Diver Easier to Defend

About the author